12 Oct Time for a mortgage restructure?

Time for a mortgage restructure?

Is your mortgage still fit for purpose? With mortgage interest rates increasing, and many borrowers’ fixed-term rates due to expire in the next few months, it’s worth looking for ways to make your home loan work better (and harder) for you.

Read on for some key steps you can take, depending on your goals. And if you’d like to learn which of these strategies is suitable for you – get in touch. We’re here to help.

Paying more than the minimum

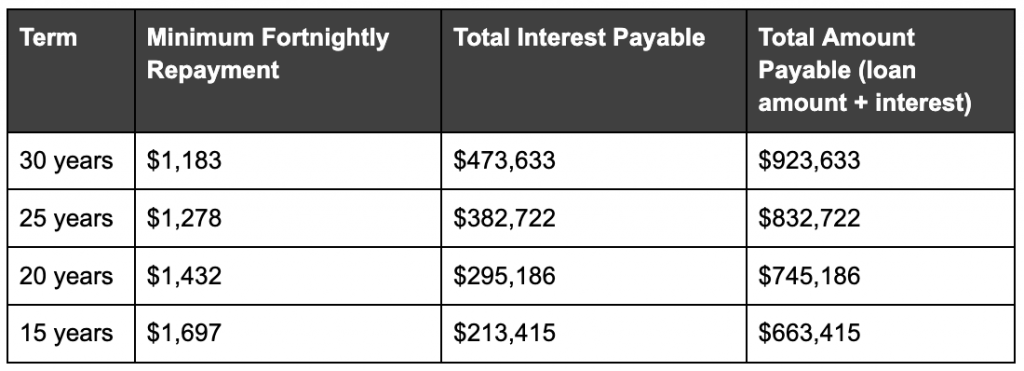

Is paying off your mortgage sooner rather than later on your priority list? Remember, the longer your mortgage term lasts, the more interest you will pay on it over time.

To give you an idea of how much difference the mortgage term makes, we ran some numbers below. For illustration purposes, we considered a mortgage balance of $450,000 at 5.5% per annum.

So, how can you reduce the term of your home loan? A key way is to pay more than the minimum, either by paying extra lump sums into your mortgage or increasing your regular payments.

How much extra you’re allowed to pay depends on the type of interest rate. If it’s a floating rate, you can add as much as you like (and can afford to) with no penalties, whereas with fixed-term rates you can only pay extra up to a certain limit without incurring an early repayment fee. Get in touch if you’d like to learn more, and remember: a fixed rate expiry can be a good opportunity to consider how you’d like to move forward.

Splitting your mortgage

If your fixed-term rate is due to expire soon, you may look at splitting it into different chunks – a mix of fixed and floating rates.

The key benefit of this option is that you can make extra repayments on the floating portion with no penalties. Plus, by fixing part of your mortgage for a longer period and part for a shorter one, you can spread the risk of future interest rate increases over different loan terms.

Do you need to lower repayments for a while?

Inflationary pressures are putting many people’s budgets under strain. So, if you’re going through a rough patch financially and find it difficult to meet your mortgage repayments, please don’t hesitate to contact us: there are options that we can discuss with you to help put in place a plan or to understand what the lender might need when you talk to them.

Just keep in mind that, while your mortgage repayments would be lower in the short term, the overall interest costs would most likely increase. Again, we can help you understand the pros and cons, and make a well-informed decision.

Do you have any questions for us?

We welcome you to contact us: when it comes to your mortgage, no question is too big or too small.

Disclaimer: Please note that the content provided in this article is intended as an overview and as general information only. While care is taken to ensure accuracy and reliability, the information provided is subject to continuous change and may not reflect current developments or address your situation. Before making any decisions based on the information provided in this article, please use your discretion and seek independent guidance.

No Comments